M&A Activity Remains Steady Through Second Quarter 2021 but a Second-Half Wave Awaits

By: Mark Crites

After what felt like a hangover during the first three months of 2021 following a blockbuster end to 2020, the mergers & acquisitions market in the insurance brokerage industry maintained its steady pace in the second quarter. Deal activity during the first six months of 2021 surpassed the same period in 2020 by 16 deals. This trend was expected following a five-year quarterly low recorded in the second quarter of 2020 when uncertainty surrounding COVID-19 was at its peak.

What has been the biggest driver of this deal volume? Two words: Private equity.

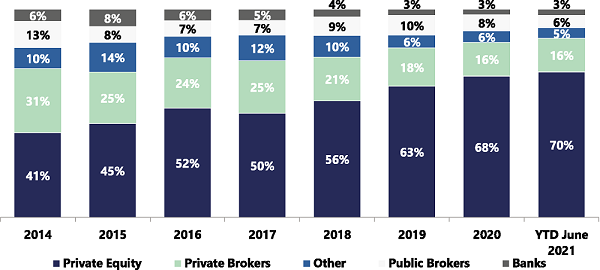

The chart below shows the percentage of deals completed by buyer type since 2014. In the first half of 2021, private-equity backed brokers have accounted for an astounding 70% of the total deal volume.

Why are institutional investors flocking to the insurance brokerage industry? Steady performance and strong operating fundamentals, such as high recurring cash flow and low cash flow requirements, have underpinned the aggressive move by investors. During the pandemic, the insurance brokerage industry has been a haven for investors compared to other industries like hospitality and retail.

But what happens next? Could 2021 deal activity really surpass 2020’s record high? Yes, it could. The uncertainty surrounding tax changes—both corporate and personal—continues to be the headliner, as it was in 2020. Here are five other reasons driving sellers and buyers to the table in 2021 that could lead to another record year:

1) Expanded buyer universe. There are now over 40 active buyers of insurance agents and brokers in the U.S., including private equity firms, compared to five in the late 1990s. Each broker has taken a slightly different strategy and sellers have more models to choose from than ever before, increasing the likelihood of finding an attractive partner.

2) All-time high valuations. Competition from buyers in our industry, coupled with the hard market, strong performance from public insurance brokers and low corporate tax rates, have kept valuations high. For example, a quality broker with $3-$10 million in annual revenues can expect to receive 10 times pro forma EBITDA at closing as a guaranteed payment, plus an earn-out opportunity of up to three times pro forma EBITDA.

3) Strong operating fundamentals. While many industries went backward during the pandemic, agents and brokers posted 4.3% average organic growth in 2020, according to Reagan Consulting’s Growth & Profitability Survey, and are on pace to post their highest organic growth in the history of the survey in 2021 of 7.0%.

4) Low-cost capital. The institutional capital available to large brokerages is greater and cheaper than ever before with interest rates at historically low yields.

5) Intense competition from high performers. With significant investments being made by the largest brokers, many private brokers are feeling pressure in the competition for middle-market clients. One way to get access to a bigger toolkit is to partner with a well-capitalized strategic buyer.

Reagan Consulting is active in the M&A market and continues to hear from several buyers that their respective pipelines are filling up as more sellers come to market. The Biden administration has made it clear that capital gains and corporate tax rate hikes are on the horizon for either late 2021 or 2022. Timing will be decided this fall with Congress back in session.

With the above dynamics at play in 2021 coupled with full buyer pipelines and expected tax rate hikes, we expect yet another record-breaking year of M&A activity for the industry.

Mark Crites is a partner at Reagan Consulting.

This month’s issue

The June issue is out now!